If you’ve been looking for a travel-focused credit card that actually saves money instead of adding hidden charges, the Scapia Credit Card has probably already caught your attention. It has quietly become one of the most talked-about cards in India, especially among frequent travelers and young users who want rewards without paying annual fees.

Issued in partnership with Federal Bank, this card is designed to keep things simple: no joining fee, no annual fee, and zero forex markup. That alone puts it ahead of many premium travel cards.

But is it actually worth using in 2026?

Let’s break everything down in detail.

What is Scapia Credit Card

The Scapia Credit Card is a travel-centric, lifetime free credit card that rewards you for both everyday spending and travel bookings.

What makes it different:

- Dual card system: Visa + RuPay

- Strong travel rewards through the Scapia app

- Zero forex charges on international spending

- Rewards even on UPI transactions

Unlike traditional cards, Scapia is built around an ecosystem where your rewards are meant to be used for travel.

Key Features and Highlights

1. No joining fee and no annual fee

Scapia charges nil joining fee and nil annual membership fee. That alone makes it attractive for users who do not want the pressure of spending thresholds just to justify the card cost.

2. Zero forex markup

One of the biggest reasons people apply for Scapia is its 0% foreign currency markup. Most traditional Indian credit cards charge around 3% to 3.5% forex markup, sometimes more after GST. Scapia removes that charge, which can make a real difference on international trips, hotel bookings, or purchases in foreign currency.

3. Travel rewards

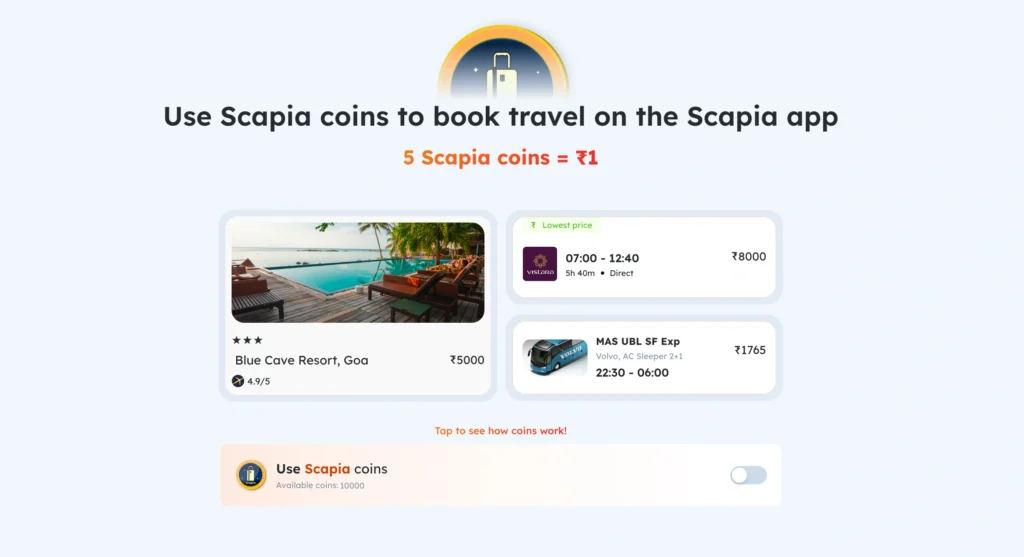

Federal Bank’s Scapia page says the card offers 10% reward on every eligible online and offline spend on Visa, and 5% reward on eligible UPI, online and offline spend of ₹500 or more on RuPay. Rewards are credited as Scapia Coins and can be redeemed instantly on travel bookings in the app. Federal Bank also states that 5 Scapia Coins = ₹1. That means the usual 10% coins earning works out to an effective base return of about 2% in rupee value.

4. Airport privileges

Scapia’s airport benefits changed in a useful way. Instead of only talking about lounge access, the card now highlights broader airport privileges:

- Unlimited domestic lounge access unlocks on a combined monthly spend of ₹20,000 across Visa and RuPay cards

- at domestic airports, you can also get up to ₹1,000 back in rewards on dining, shopping, or spa spends after meeting the same spend trigger

- for international terminals in India, Scapia says you can get up to ₹2,000 back in rewards for duty-free shopping or dining, unlocked with every ₹50,000 international flight booking on the Scapia app, effective 27 February 2026

That is an important distinction. Scapia is strong for domestic airport use, but it is not the same as unlimited international lounge access in the usual premium-card sense. If that is your top priority, you should know this before applying.

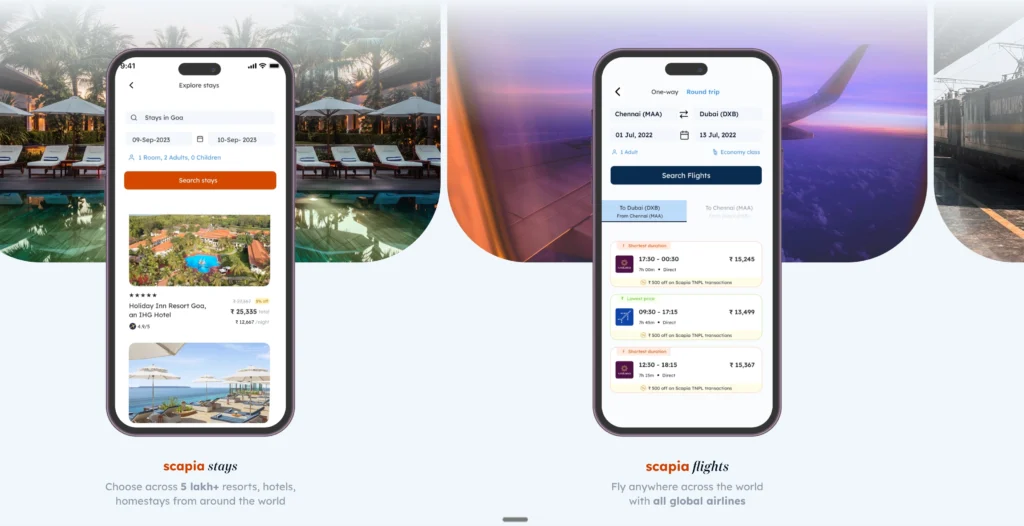

5. Strong app integration

The card is tightly linked to the Scapia app, where you can manage repayments, set limits, control permissions, track rewards, and redeem coins for flights, hotels, and buses. Federal Bank also notes that onboarding is fully digital, the virtual card can be activated immediately after approval, and the physical card typically reaches you in 2 to 5 days. Scapia’s Google Play listing also shows heavy adoption, with 10 lakh+ downloads and tens of thousands of reviews, which suggests the app is not a side feature but the centre of the whole product.

Scapia Credit Card Key Highlights

| Feature | Details |

|---|---|

| Card Type | Travel Credit Card |

| Issuer | Federal Bank |

| Joining Fee | ₹0 |

| Annual Fee | ₹0 |

| Forex Markup | 0% |

| Rewards | Up to 20% on travel |

| Lounge Access | Unlimited domestic (spend-based) |

| Interest Rate | ~3.75% per month |

| Best For | Frequent travelers |

Scapia Credit Card Fees and Charges (Detailed)

Complete Pricing Table

| Charges Type | Amount |

|---|---|

| Joining Fee | ₹0 |

| Annual Fee | ₹0 |

| Forex Markup Fee | 0% |

| Interest Rate | 3.75% per month (~45% annually) |

| Cash Advance Fee | 2.5% or ₹500 |

| Late Payment Fee | Up to ₹1,000 |

| Overlimit Charges | 2.5% |

| Card Replacement | ₹200 |

Rewards Structure Explained

Scapia rewards are issued as Scapia Coins. Federal Bank says rewards can be redeemed instantly on flights, hotels, and buses in the Scapia app, and the official site states 5 coins = ₹1.

1. Base Rewards

- 10% rewards on Visa card spends

- 5% rewards on RuPay spends above ₹500

- Minimum transaction required for rewards

2. Travel Rewards

- 20% rewards on travel bookings via Scapia app

- Applies to flights, hotels, buses, and more

3. Coin Value

- 5 coins = ₹1

- Example: 100 coins = ₹20

So effectively:

20% reward = ~4% value

10% reward = ~2% value

Pros and Cons

Pros

- Zero joining and annual fee

- 0% forex markup, which is excellent for international spending

- Easy-to-understand rewards

- Domestic airport privileges after meeting spend criteria

- Fully digital onboarding

- Immediate virtual card activation after approval

- App-based controls, repayments, and redemption

- Good fit for young travelers and first travel card users

Cons

- Rewards are strongest only if you redeem through the Scapia app

- No broad premium-style international lounge program by default

- Lounge and airport benefits require monthly spend thresholds

- Revolving interest rate is high at 41.88% p.a.

- Travel redemptions are convenient, but you are staying inside the Scapia ecosystem rather than getting flexible airline miles or hotel points

Eligibility Criteria

Scapia’s official public pages do not clearly publish a detailed salary threshold on the main card page. What is clearly stated is that the process is app-based and digital. Third-party financial platforms generally describe the expected profile as an Indian resident adult with a good credit profile, with a common benchmark of around 750+ credit score and age minimums typically starting from 21 years for unsecured cards. Some also mention a minimum annual income of around ₹5 lakh, but that is not clearly published on the official Scapia page, so treat it as a market estimate rather than a guaranteed official rule.

A practical way to think about it:

- Age: usually 21+ is safer for unsecured cards

- Credit score: 750+ improves your chances

- Income: a stable salaried or self-employed profile helps

- Documents: PAN, Aadhaar, and KYC details are typically required

Application Process

Applying for Scapia is straightforward and mostly app-led.

Step by step

- Download the Scapia app

- Tap Apply Now

- Enter your basic personal and financial details

- Complete identity verification and KYC

- Wait for the credit assessment

- If approved, activate the virtual card immediately

- Receive the physical card in around 2 to 5 days

Approval time

Federal Bank says the card can be issued through a fully digital onboarding process in minutes, while the virtual card can be activated immediately after approval. In practice, approval timing can vary depending on verification, bureau checks, and applicant profile.

Comparison with Other Cards

Here is a simple comparison with a few well-known alternatives.

| Feature | Scapia | Niyo SBM Credit Card / Zero Forex Card | OneCard |

|---|---|---|---|

| Joining fee | Nil | No joining fee | Nil |

| Annual fee | Nil | Nil on SBM credit card | Nil |

| Forex markup | 0% | 0% | Around 1% |

| Rewards | Travel-focused Scapia Coins | Niyo Coins and travel discounts | 5X on top categories |

| Lounge benefit | Domestic airport privileges with spend trigger | International lounge access with spend criteria on eligible Niyo cards | Not the main reason to get the card |

| App experience | Strong travel-first app | Strong travel app | Strong spend-management app |

| Best for | Domestic travelers and zero forex seekers | International travelers who want zero forex | Everyday users who want a lifetime free metal card |

Scapia is unique because it mixes three things very well: lifetime free pricing, zero forex markup, and a clean travel redemption system. Niyo is stronger if your priority is international travel tools and global lounge-linked benefits. OneCard is more of a smart everyday card with low fees, app control, and low forex, but it is not as travel-centric as Scapia.

Who Should Get This Card?

Scapia makes the most sense for:

- people who travel a few times a year and want a simple travel card

- students or young professionals building a card setup for future travel

- users who want zero forex without paying premium annual fees

- people who prefer an app-first experience over old-school reward portals

- travelers who spend enough monthly to unlock airport privileges

You may want to skip it if:

- you want airline miles or hotel transfer partners

- you need automatic premium international lounge access

- you usually prefer cashback over travel redemptions

- you tend to carry balances month to month

Final Verdict 2026

In 2026, the Scapia Credit Card remains one of the most practical travel cards for Indian users who want value without complexity. The biggest wins are obvious: no joining fee, no annual fee, zero forex markup, decent travel-centric rewards, and a polished app experience. Those benefits are real, and for many users they are more useful than flashy premium-card promises.

Its main limitation is that the rewards are most valuable inside the Scapia ecosystem, and the airport benefits are strong for domestic travel but not a full premium international lounge package. Also, like any credit card, the high revolving interest rate means you should never carry unpaid balances if you can avoid it.

Bottom line

Scapia is worth considering if you want a beginner-friendly, travel-focused, zero-forex card in India without annual fees. For frequent international luxury travelers, there are better premium cards. But for most practical users, especially younger travelers and cost-conscious flyers, Scapia is still one of the better value options in the market right now.